The argument against holding bonds: Your portfolio is better off without them over the long haul

Studies have shown that, when it comes to investing, most people make decisions based on intuition rather than reasoning. They focus primarily on the possibility of a loss (rather than the probability of a gain), and tend to contemplate the immediate future rather than taking a long-term view.

Together, these behavioural biases drive people to invest a disproportionate share of their capital in an asset class that makes absolutely no sense for long-term investors – particularly in today’s environment. That asset class is bonds.

At this point, you may be thinking that bonds are far less risky than stocks and, therefore, they have a place in every portfolio. It is true that, in the short-run, the market price of bonds tends to be less volatile than the market price of stocks. Thus, the idea of a “balanced” portfolio, consisting of both stocks and bonds, sounds wonderfully comforting.

The more you think about it, however, the less comforting it becomes.

Let’s go back to basics. Investing is laying out money now in the expectation of receiving more money, in real terms, well into the future. The phrase “in real terms” refers to the inevitable decline in the purchasing power of a dollar, because of inflation. In Canada, it takes about $1.46 today to buy what $1 did 20 years ago. The inflation rate over this time period was about 1.9 per cent per annum.

If, over the past 20 years, you owned a portfolio of 10-year Government of Canada bonds, you received an average yield of 3.6 per cent a year. If you paid tax at a 50-per-cent marginal rate, your bonds would, after tax, have produced an annual return of 1.8 per cent – less than the rate of inflation. So, after both tax and inflation, you would have lost money.

In addition, any increase in longer-term interest rates will result in a fall in the market value of bonds. The longer the remaining term to maturity of the bonds, the greater the sensitivity of market price to changes in interest rates. One cynic has said that instead of providing risk-free returns, bonds actually provide return-free risk.

For most people, the obvious alternative investment to bonds is stocks. While a bond is simply an interest-bearing IOU from the issuer of the bond to the investor, a stock is a piece of ownership in a business. An investment in a productive asset such as a business should, unlike a bond, be able to deliver profits that will keep up with or exceed inflation. Stocks should, therefore, over time, represent a better investment than bonds.

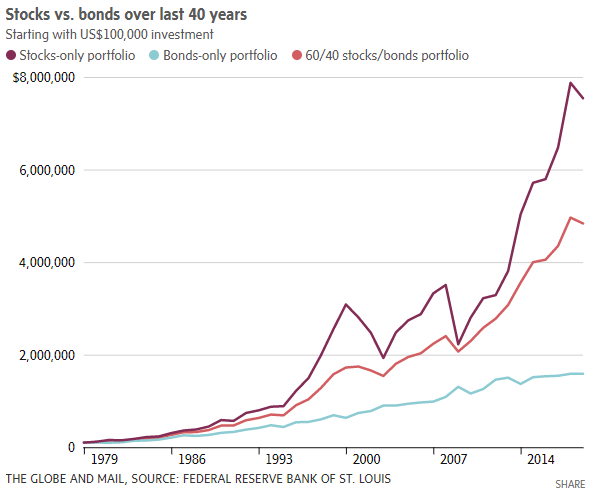

If we are right about this, it should show up when we examine the total long-term returns on stocks and bonds. The U.S. numbers (provided by the Federal Reserve database) are more complete than the Canadian equivalents and include a broader range of sectors. We looked at three portfolios over the past 40 years, each valued on Jan. 1, 1979 at US$100,000. The first contained the stocks in the S&P 500 Index, the second consisted of the return on U.S. 10-year Treasury bonds and the third was a balanced portfolio with a typical weighting of 60-per-cent stocks and 40-per-cent bonds, rebalanced annually.

While stocks were more volatile, the stock portfolio finished well ahead. By Dec. 31, 2018, the value of the bond portfolio reached US$1.59-million. The balanced portfolio rose to US$4.84-million. And the stock portfolio finished at US$7.54-million (more than four times the value of the bonds). The same would be true over almost any long-term period.

Looking at a long time period such as 40 years is important. It provides statistically relevant data, which enables you to more accurately estimate the likely outcome of any action you might take. Also, your ability to live comfortably will depend on the return provided by your investments for the rest of your life. This includes your retirement, which is likely to last more than 20 years. Cash flow obtained from a combination of dividends and realized capital gains is taxed at a far lower rate than interest from bonds.

So, what is the argument for owning bonds? Primarily, peace of mind. While experienced investors know that short-term fluctuations in the price of stocks are to be expected and tolerated, those fluctuations cause angst for most of us.

How should we minimize this angst? In our view, not by investing in a so-called balanced portfolio of stocks and bonds. Rather, we suggest you invest an amount equal to, say, three years of estimated living expenses in a “buffer” account that holds short-term cash equivalents such as one-year guaranteed investment certificates.

Unlike a portfolio of bonds, the value of your GICs will not fluctuate with interest rates. If you are taking funds from your investment account to cover living expenses, withdrawals can be made from this buffer account. The buffer account can be topped up from the stock portfolio each January, so long as your stocks have performed well the previous year. After a down year in the stock market (which happens about one in four years), you can delay the top-up until things improve. Maintaining the buffer account will, of course, reduce the long-term return on your assets. But the peace of mind it provides may make it worthwhile.

Choosing the right asset class is your most significant investment decision. Those who get it right will be rewarded with a far more comfortable retirement.