At first blush, sports may not appear to have much in common with investing. But beyond being something to watch or participate in, sports can hold lessons for investors about achieving success over the long-term.

This summer, the Paris Olympics demonstrated the unpredictability and randomness of outcomes across different sports. Sports with more variables such as players, nets, posts and penalties are generally less predictable.

Sports with repetitive and objective events and relatively few variables have more predictable outcomes (think more points per game and more games per match). The outcome of any single point may be random, but it is relatively predictable that the more talented individual or team will win over the course of the competition.

As in sports, the short-term performance of the stock market is largely random. In the long-term, though, the key to success in both sports and investing is about putting the odds in your favour.

Tennis is a good parallel to investing. In a sport with fewer variables than most (often only two players and one ball) and many points required to win a match, career statistics from one of the greatest players ever demonstrate the power of compounding and consistency over the long-term.

In a recent commencement speech at Dartmouth, tennis great Roger Federer highlighted that he won only 54 per cent of the points over the 1,526 singles matches he played during his professional career. However, his small points-won advantage led to him winning about 80 per cent of his matches.

Mr. Federer’s winning percentage over his long career from 1998 to 2022 amounted to 103 singles titles, making him one of the most successful male tennis players ever. Yet, even with his talent, if Mr. Federer’s career had lasted only a few seasons, he would likely be a mere footnote in tennis history.

In investing, it is unrealistic to think that you will make performance-enhancing decisions even 60 per cent of the time. Many investors find this fact, and the fact that they will regularly make bad investment decisions, difficult to accept. However, like Mr. Federer, if you can consistently tilt the odds even slightly in your favour, it will lead to significant outperformance over time. The difference will likely not appear material in the early years, but can become very powerful later on.

Small advantages can make a big difference over time, but they are unlikely to play out consistently. In 24 years, Mr. Federer won 20 major titles – the Australian, French and U.S. Opens and Wimbledon. But in 14 of those years, he did not win a single major title.

Similarly, the share prices of even top-performing businesses do not outperform or even go up every year. As one example of a company with a stock that has outperformed over the long run, Amazon.com Inc. produced an annualized total investment return of 22.5 per cent over 20 years up to the end of 2023, more than doubling the S&P 500′s 9.9-per-cent annualized total return over the same period.

Despite this overall return, Amazon’s share price fell in six of those 20 years, in a period when the market fell in only three of the 20 years. In addition, Amazon underperformed the S&P 500 in nine of the 20 years, or 45 per cent of the years.

Many investors who owned shares of Amazon and other great companies 20 years ago may have sold them by now. For those investors, the long-term power of compounding has been interrupted by, for example, impatience or fear in response to a year in which the share price fell. This type of behaviour is one of the key reasons why most investors, including professionals, find it difficult to outperform the market over the long-term.

When you believe that you have purchased a piece of a great company at a reasonable price, you will generally be better off continuing to own it for the long run. This will tilt the odds in your favour by allowing your capital to compound, as Roger Federer’s playing statistics did over the course of his tennis career.

In discussions about artificial intelligence, we often hear the question: Why do neural networks, designed to think like us, generate incorrect information? We don’t know – in part because we don’t know much about how the human mind works.

Perhaps the greatest expert on human cognition is Daniel Kahneman, a psychologist who won the Nobel prize in Economics in 2002. In his book, Thinking Fast and Slow, he points out that, in some areas of life, our minds tend to lead us in the wrong direction.

To illustrate, consider Frank, who lives in Toronto. He wears glasses and loves reading. Is it more likely he is a librarian or a salesman? Most people answer librarian. However, there are more than 100 salesmen in Toronto for every male librarian, so the correct answer is salesman. Once the reasoning behind this outside view is explained, most people understand why salesman is the correct answer. However, I suspect they are somewhat uncomfortable with this approach.

That’s because we are all hardwired to prefer stories to numbers. For most of human existence, stories bound us together. These stories inevitably included a cause and effect, making the world appear ordered and predictable. Randomness was an unknown concept; thinking in terms of large numbers and probabilities was not required. Our minds have not yet evolved in that direction.

Mr. Kahneman points out that thinking probabilistically requires slowing down and thinking hard about the question. We make thousands of decisions every day, and this is completely unnecessary for almost all of them. However, in a few areas of modern life, it is a crucial skill – and that includes investing.

Successful stock-market investing results from buying companies for less than their true value. Because that true value is a function of the company’s future profits, your job as an investor is to forecast those profits as best you can.

Most investors will base their forecast on some combination of their knowledge of the company and their past experience. In effect, they look at what they perceive as the company’s key features and produce a narrative about its likely future, an approach psychologists call the inside view. Some people are better at this than others, but we all suffer from over-confidence in our ability to predict the future. For the vast majority of people, this intuitive, subjective approach is unlikely to result in superior results.

Mr. Kahneman states that there are three types of information relevant to a prediction: the outside view, based on evidence of similar situations; the inside view, based on the specifics of the case; and the relative weights you should assign to each.

One way to determine the appropriate weighting of the outside and inside views is to know where the activity lies on the luck-skill continuum.

For activities where skill dominates (such as a chess game or running race), the outside view has little or no bearing. By contrast, when randomness (luck) dominates (such as playing a few hands of gin rummy) the probability of the outcome will be based primarily on the outside view.

Where an activity falls on this continuum can be measured by studying the consistency of results over time. If skill dominates, results will be mostly (or entirely) the same. If randomness plays the dominate role, results will be all over the place.

As discussed in a previous ROB article, Michael Mauboussin, author of The Success Equation, has examined the results of more than 1,400 mutual funds, comparing their results, relative to the average, between two successive three-year periods. (Three years is the most common period of time over which to evaluate an investment manager’s performance.) In this comprehensive study, he discovered a startlingly low correlation between the performance achieved by each fund in the two periods.

Mr. Mauboussin concludes that success in investing, measured over a three-year period, is an activity that is about 85-per-cent luck (randomness) and only 15-per-cent skill. (In fairness to professional investors, it should be noted that, for longer time periods, skill would have a higher weighting.)

Based on this study, Mr. Mauboussin points out that, when investing, the outside view should be given the greater weight.

How do you do this? Before predicting how a particular business is likely to do, learn how similar companies have performed in the past.

To take a somewhat over-simplified example, if you are looking at a consumer-packaged goods company with annual sales between $1-billion and $5-billion, begin by asking what has been the average five-year annual growth in sales of companies falling in this category. This information is increasingly available. Let’s assume it is 6-per-cent per annum. If you had predicted that the company you are looking at will grow at 14-per-cent per annum over the next five years, you should perhaps temper your optimism.

However, if you had first come to that conclusion based on an inside view, you will likely resist this. We all suffer from confirmation bias, which inclines us to ignore contradictory evidence. You may reply indignantly that there is no reason to think that a particular company cannot greatly outperform the long-term average. This is true, just as it is possible Frank is a librarian. But, in both cases, you are simply following a very human inclination to ignore probability.

Successful investing is not about hunches, instincts or intuition. It is about having the discipline to tilt the odds in your favour. One way to do this is to put things in the proper order. Start with the outside view: Step back and see a company first as being a member of a representative group. Then, by all means, consider its particular qualities before deciding to buy, sell or hold.

It’s not easy, but those who can do this consistently (perhaps with the assistance of a neural network) will be rewarded.

This spring marked the 50th anniversary of a great sporting event – Secretariat’s Triple Crown win. Photos taken near the finish line at the Kentucky Derby show the jockey, Ron Turcotte, looking back and seeing no horses anywhere near him. Secretariat was a phenomenal horse and Turcotte, who controlled how fast he came out of the gate and decided whether to set the pace or conserve energy for a late push, was a great jockey.

In investing, the analogy to a horse and a jockey is a business and its CEO. An outstanding long-term result requires both an exceptional business and excellent management.

If you question whether the intelligence and integrity of a company’s leader is an important determinant of investment returns, think of companies like Enron and WorldCom.

When true investors buy a stock – a piece of a business, in other words – their goal is to achieve a superior return over the long run. It follows that they should look for a CEO who is likely to create long-term value for the shareholders.

How do you identify such a CEO? In addition to past performance, there are a number of characteristics to look for – and to avoid.

One place to start is public disclosures. If management commentary is highly promotional, you should probably think twice before investing. When management proclaims their company’s stock is undervalued, you should ask why they are making that statement. Similarly, if the accounting treatment appears aggressive or inconsistent, that is a red flag.

Conversely, when management speaks to you as an owner, in a straightforward manner, it’s a good sign. Ideally, the CEO will disclose the long-term goals that management has set, and explain how you might reasonably calculate changes in the company’s economic value. Two CEOs who do this regularly, and with a high degree of sophistication and humility, are Warren Buffett of Berkshire Hathaway and Mark Leonard of Constellation Software.

You should also look at other factors such as how long managers have worked there, how much of their net worth is invested in the company, and how their compensation is calculated. Charlie Munger has said, “Never, ever, think about something else when you should be thinking about the power of incentives.”

Are management incentives tied to the long-term performance of the business (a good thing) or to the current stock price (a bad thing)?

While stock-based compensation can be used to retain management and foster a sense of ownership, stock options dilute your ownership. Furthermore, most options are not well designed. If a company issues options, management’s ability to exercise them should be conditional on longer-term operational targets having been met. Also, management should be obliged to hold at least some of the shares for a few years after the options are exercised.

A CEO’s most important role is capital allocation. How are profits employed? Through a repayment of debt? Reinvestment in the business? Acquisitions? Dividends? Stock buybacks? In his book, The Outsiders, William Thorndike describes the extraordinary effect intelligent capital allocation can have on shareholder value.

How have past acquisitions and divestitures affected profit per share? Also, what is the track record of management when it comes to stock buybacks?

Buybacks are not created equal. Every company has an economic or intrinsic value, which can be roughly estimated. The market price of the stock is often well above, or below, that value. If a company buys back its shares for less than their economic value, it is positive for the shareholders. If it pays more than economic value, it is negative. It’s surprising how few CEOs appear to understand this. A good question to ask any CEO is “How do you think about stock buybacks?” Often, the answer speaks volumes.

Over the past several decades, investors have obtained access to more and more quantitative information on listed companies. As market participants increasingly rely only on numbers, you will do well to examine other aspects of the business – and to begin by assessing management.

Don’t bet until you know both the horse and the jockey.

Are you a good investor? Or, to ask exactly the same question differently, how good are you at predicting the future?

Making an investment decision is no more or less than making a forecast.

The stock market price of a company reflects the collective expectation of thousands of investors about the future profits of that company. If you are to succeed as an investor, you must do a better job than the other market participants of forecasting those profits.

We all want to know the future – and not only in the context of investing. This demand is met by a plethora of pundits expounding on what will happen next. We seldom measure the accuracy of those predictions.

Very few of us can forecast competently. To quote the economist John Kenneth Galbraith, “We have two classes of forecasters: those who don’t know – and those who don’t know they don’t know.”

Of greater concern, we are perpetually overconfident in our ability to predict the future.

The good news is that all investors can sharpen their forecasting skills. An excellent place to start is the book Superforecasting: The Art and Science of Prediction, by Philip Tetlock and Dan Gardner.

Prof. Tetlock, a professor of psychology at the University of Pennsylvania, spent decades studying the accuracy of economic, social and political predictions made by experts. Nearly all the experts had advanced degrees, and half had PhDs. The results were shockingly poor. The expression he used was “roughly as accurate as a dart-throwing chimpanzee.”

Furthermore, there was an inverse correlation between the fame of the forecaster and the accuracy of their prediction. The best-known pundits tended to craft a compelling narrative in a confident manner rather than accept the complexity of the situation. Because we all like simple stories, these people are most in demand – in print or on the screen. They are often wrong. But never in doubt.

After the failure of the U.S. intelligence community to predict the events of Sept. 11, 2001, and the lack of weapons of mass destruction in Iraq in 2003, an American agency called the Intelligence Advanced Research Projects Activity decided to launch a forecasting tournament, open to the public, with a view to improving their own predictive ability.

As part of this program, Prof. Tetlock and a few colleagues launched the Good Judgment Project. This was one of several teams that would compete to make accurate forecasts.

Starting in 2011, the U.S. intelligence agency posed approximately 500 questions about possible economic and political outcomes. The result, over the following four years, was more than a million individual predictions. The accuracy of these forecasts was measured using a Brier score, a scale originally designed for meteorologists.

Prof. Tetlock’s group beat the control group by about 70 per cent. The top 2 per cent in his group were dubbed the Superforecasters.

Prof. Tetlock studied the approach of this elite group and concluded that accurate foresight is a real and measurable skill. Furthermore, it can be learned and cultivated.

How can investors and others improve the accuracy of their predictions?

Look for people who are intellectually curious and highly numerate, and have above-average intelligence.

Even more important than IQ is RQ or rationality quotient, a test established by professor emeritus Keith Stanovich at the University of Toronto. Those with high RQs take an “outside view” and think in terms of probabilities. Most people, including most professional investors, find it hard to think this way.

Investors should also find people who are “actively open-minded.” In other words, they should consider multiple points of view and be slow to assign causality. They also have a growth mindset – they want to work at improving their technique. Prof. Tetlock has said that if he had to reduce superforecasting to a bumper sticker, it would read: “Beliefs are hypotheses to be tested, not treasures to be guarded.”

And they should allow forecasters to work collaboratively in teams.

If you are one of those forecasters, avoid relying on your instinct. Force yourself to fully reflect on the question at hand, and be willing to change your view as facts change.

Predicting the future success of a company is not an easy task. Only a small minority of professional investors beat the market averages, after fees, over any 10-year period.

Perhaps, however, if you follow Prof. Tetlock’s advice, you will be among that illustrious minority. You will be one of the Superinvestors.

The beginning of the new year is an ideal time to update your financial plans and, if you are in a position to do so, contribute to your investments. For young people in particular, maximizing the time that your capital has to compound will make a significant difference to your wealth over time.

When investing, most people focus on the return that they earn while underestimating the importance of a long, uninterrupted investment runway. The story goes that, when asked why he had not spent the money he had been given to get a haircut, a teenage Warren Buffett replied, “Why would I want a $300,000 haircut?” Even at a young age, Buffett understood that if, in addition to the return on your initial investment, you earn returns on your returns, the growth in your capital becomes exponential over the long run.

If you are just starting out, here are some basic investment guidelines to assist you in maximizing your long-term wealth and your financial optionality along the way. All of them are simple, but not easy.

Start saving early and save regularly

Saving often seems difficult, particularly for young people. Starting with small, regular amounts can make it easier to begin and for it to become habitual. It might help to set aside part of your monthly salary or annual bonus. It might also help to have the savings bypass your chequing account and go directly into your investment account – the funds will not be ‘seen’ and there will be no temptation to spend them.

The sooner you start saving, the greater the power of compounding. If you invest $1,000 at age 25 and earn 9% a year for 40 years, by the time you turn 65 it will be worth more than $31,000. In contrast, the same amount earning the same return, but invested at age 35 for 30 years will be worth only about $13,000.

In addition, adding to your savings on a regular basis is powerful. Using the example above, if you invest $1,000 each year from age 25 for 40 years, the $40,000 invested will grow to almost $370,000.

Invest to match your goals and time horizon

Everyone’s investment approach should suit their personal situation and the purpose of the capital that they are investing.

If your long-term goal is to build a capital base capable of providing future cashflow and a security net, your objective should be to grow it safely at a rate that is above inflation on an after-fee and after-tax basis. Buying pieces of high-quality companies that will be around and worth more in the years to come (i.e. stocks) is a proven way to do this.

In any given year, stock market returns are random and markets regularly have down years – most recently in 2022 and 2018. However, stock market returns are relatively predictable over the long run (10 years or more). In the United States, the stock market has produced attractive annualized long-term total returns of about 10% before fees for more than a century.

Not investing appropriately is risky, particularly for someone with a long investment horizon. A young person, saving regularly and investing at an annualized rate of 9% (as above), will earn three times more from age 25 to 65 than if they decide to ‘play it safe’ and invest in a way that earns an annualized return of 5%.

Maximize your time in the market, don’t try to time the market

One thing that has not changed in the past century is that most investors tend to buy stocks when they are going up and sell them when they are going down – the opposite of what they should do.

Studies show that, because of buying and selling at the wrong times, investors in, for example, index funds consistently underperform the index the funds are tracking by a much wider margin than the fees they are paying.

The reason for this is because the short-term volatility of the stock market makes people emotional, both greedy and fearful. Many investors also like to believe that, when the market begins to fall, they can get out and then be smart and brave enough to reinvest when it has bottomed. Unfortunately, they only see the bottom after it has passed. No matter what anyone says and how many forecasts are made, stock markets are not predictable in the short-term. Also, the best periods in the market often follow the worst periods and have a disproportionate impact on your overall long-term return.

The solution? Only invest as much money in stocks as allows you to sleep at night and keep that capital invested through thick and thin.

Keep your costs low

Taxes and fees are forms of negative compounding on capital – in the short run, their impact may not feel material, but in the long run it can be significant.

Staying invested, and not trying to time the market, has the added advantage of resulting in lower turnover (trading) in a portfolio. Low turnover reduces the realization of capital gains and, therefore, taxes owed in taxable accounts as well as transaction costs across accounts.

Investing in low-fee ETFs can help to reduce fees. Or, if you decide to use an investment advisor, make sure, amongst other things, that their fees are reasonable.

Take advantage of your tax-sheltered accounts

Tax-sheltered accounts such as RRSPs, TFSAs and FHSAs allow capital invested inside of them to compound tax-free. They provide an investment advantage that should be utilized to the maximum extent possible.

If you are earning a good salary and can find the means to do so, contributing to your RRSP and/or FHSA first will probably make the most sense, as the tax credit received will reduce income tax owed. If you are fortunate and have surplus savings after having fully contributed to your RRSP and/or FHSA, then you should also contribute to your TFSA.

The maximum annual contribution to a TFSA is $7,000 in 2024 – often not large enough for people to focus on making it every year, let alone early in the year, without realizing the long-term consequences.

However, making $7,000 annual contributions starting at age 18 (the earliest year for contributing) until age 65, and assuming an investment return of 9%, the total contributions of just about $330,000 will grow to some $4.5 million. Think of it like building a pension.

For parents reading this article, helping your child make their TFSA contributions in the early years is an amazing gift. The contributions made from age 18 until 30 (12 years) will be worth more than all of those made from age 30 to 65 (35 years) due to the power of compounding capital over the longest possible period of time.

If you earn enough to save and live a long, healthy life, the ability to achieve financial independence in retirement, and to have financial flexibility along the way, is largely in your hands.

Norman Rothery’s ranking this past weekend of the 250 largest stocks on the TSX pointed out the advantages of tilting the odds of investment success in your favour by focusing on company-specific financial measures (called factors). Mr. Rothery focused on both value factors, such as a low ratio of share price to earnings per share (the P/E ratio), and share-price momentum. As was pointed out in the article, combining value and momentum improves the chances of investment success.

Other factors that have been proven to improve long-term returns include size of the company and shareholder yield. The largest 20 per cent of companies in any stock market tend to underperform. And companies that pay healthy dividends and/or buy back their own shares are more likely to outperform.

Yes, of course there are exceptions to these general rules. In each case, this is only true on average when looking at a large sample size over time. But that is exactly how you determine probabilities.

When using factors, you are taking an outside view. Instead of looking at a particular business and forecasting its future, you are looking at a very broad range of companies and looking for connections between their financial characteristics and future increases in their stock price. Because there is a strong long-term correlation, as well as a logical causation, between certain factors and future investment returns, it is reasonable to conclude that by following this approach, you are increasing the probability of outperforming the stock market average.

The ability to think probabilistically is crucial. This is how Warren Buffett’s partner, Charlie Munger, has graphically described its importance: “If you don’t get this elementary, but mildly unnatural, mathematics of elementary probability into your repertoire, then you go through a long life like a one-legged man in an ass-kicking contest.”

As you would expect, combining several factors has been proven to further improve returns.

Focusing purely on factor investing for both buying and selling stock has proven successful for tax-sheltered entities such as pension funds and insurance companies. If you pay taxes, however, the resulting high portfolio turnover (frequent buying and selling of stocks) would increase your average tax rate.

To avoid this, taxable investors can elect to use factors only to define which companies they will consider investing in – and not be in a rush to sell the companies they purchase. You might, by way of illustration only, say, “I will only consider buying companies that are trading at a P/E ratio of less than 20, that have a history of buybacks or dividends providing a shareholder yield of at least 2 per cent per year, have a market capitalization of less than $50-billion, and have a return on equity (ROE) of greater than 16 per cent.” Once the field has been narrowed to companies that are more likely to outperform, you can consider other characteristics, such as debt levels, historical growth in revenue and profits, and your view of the competence of management, before deciding whether to buy.

This approach will not result in outperformance every single year, but over time it has, and likely will in the future. Most importantly, in every given year, and for every given purchase, it tilts the odds in your favour.

Unfortunately, investing in this manner runs counter to human nature. People find it easier to think about a single example than about a large sample. A quote often attributed to Stalin identifies this, perhaps inadvertently: “One death is a tragedy. A million deaths is a statistic.”

Many people believe they can predict a company’s future, and often confuse anecdotes with evidence. “If we followed those rules, we would never have bought Amalgamated Consolidated Widgets, which was a winner!” Correct. But that doesn’t change the fact that following the rules would have produced a better long-term result for the portfolio. Or that buying Amalgamated Consolidated was somewhat like winning at the roulette table in Las Vegas. The odds were against you and the happy outcome was based on luck, not skill. Over time, anyone operating with the odds against them will be disappointed.

Just to hammer home how difficult thinking this way is for most people, let’s take another example from everyday life. Your friend Frank buys a lottery ticket. You point out that the purchase was a mistake because the odds were dramatically against him. He replies that either he’ll win or he won’t. And once he knows whether he won, the odds will be irrelevant. Perhaps you instinctively agree with Frank’s view. Most people see no reason why a sample size of one is not sufficient to draw a conclusion. However, if you don’t adjust your thinking about future outcomes to focus on the probable, rather than the actual, result, you will never enjoy the benefit of going through a long life with the odds in your favour.

All of us are hard-wired to think short-term. Most people who do adopt an objective approach and know rationally that the strategy will succeed over time will abandon it if it does not produce the desired result in the first year or two.

Identifying the correct evidence-based approach is important. What is harder is having the discipline to execute that approach and stick with it through hard times.

What is the ratio of luck to skill in the following pursuits: picking lottery tickets, running a race and investing?

Most people would say that picking lottery tickets is all luck. And that the result of a running race is all ability. But what about investing?

The best-known expert in this area is Michael Mauboussin, whose fascinating book, The Success Equation, analyzes luck and skill in sports and in investing.

Mr. Mauboussin first analyzes team sports. He begins by plotting on a graph the results that would be achieved by NFL teams if the result were determined entirely by luck. As those who have studied statistics might expect, the line produced by randomness is a bell-shaped curve.

Pivoting to the assumption that only skill matters, he then plots the result that would be achieved if we were to assign different levels of skill to each team and the more skilled team won every game. The result of this skill-only assumption is a horizontal line.

Then Mr. Mauboussin compares the actual results achieved over several NFL seasons with his two studies and concludes that the result in an NFL game is determined roughly 52 per cent by skill and 48 per cent by luck. (Further studies reveal that basketball games are more skill-based than football whereas hockey is more luck-based.)

You may be wondering whether this ratio of skill to luck in sports has been constant through the years. Studies show that, over time, while the absolute performance of athletes has improved, the relative performance of the winner has declined. For example, the difference in time between the fastest and 20th fastest marathon runner in the Olympic Games has significantly decreased.

In almost all sports, the difference between the best player and the median player has dropped, owing to what has been called the paradox of skill. Essentially, as all athletes get better at their sport, the difference between the best player and the average player decreases.

In any competitive endeavour that involves both luck and skill, as the difference between the top competitor and the median competitor declines, skill becomes less important and the role of luck increases.

Investing in the stock market, like sports, is a competitive activity. Every time you buy or sell a stock, someone is on the other side of that transaction. On each trade, only one of you can be the winner.

Turning to investing, Mr. Mauboussin examines the results of more than 1,400 mutual funds, comparing their results between two successive three-year periods. He discovers a surprisingly low correlation between performance achieved by each fund in the two three-year periods. Plotting these returns on a graph would result in a picture far closer to a bell curve than a horizontal line. Mr. Mauboussin concludes that success in investing, measured over a three-year period, is an activity that is about 85 per cent luck and only 15 per cent skill.

It’s not that investors – be they professional or retail – lack skill. The result is explained by the paradox of skill – as investors have become more sophisticated and have more information available to them, the variation in ability has shrunk and results have been increasingly determined by luck.

But here’s the thing. The importance of skill varies directly with the time period studied. Results over periods of less than three years would be even more determined by luck, whereas longer-term outcomes would be more determined by skill. A 10-year track record tells you far more about a firm’s ability than a five-year track record.

The important role of randomness in investing is not bad news for serious investors. Skill does have an important role to play – but only in the long run. If you are an investor, it’s important to take a long-term view, and tilt the odds in your favour.

In any activity that involves both luck and skill, such as bridge, poker and investing, you should focus not on recent results, but rather on process – procedures that have proven, over time, to work. Mr. Mauboussin identifies several of these.

Thinking in terms of probabilities is not intuitive, but it is useful. Given our instinct to focus on whatever we have most recently looked at, it’s helpful to step back and take a wider perspective – what some call taking an outside view. For example, when forecasting future profits of a company, don’t restrict your research to how the company has grown earnings over the past few years. Instead, ask, for example, how companies of about that size, and in the same industry, have done over the past 10 years. Your final decision should be based on a synthesis of the two approaches.

Another helpful procedure is to be rigorous in your use of checklists to ensure you perform all the necessary tasks before a buy or sell decision. There’s a reason airline pilots do this.

Making investment decisions in small, cognitively diverse teams, rather than by a single individual, has also been shown to improve results.

In every aspect of life, randomness (or luck) is a far more important force than most people realize. Recognizing its role in investing will make you a better investor.

In 2005, the novelist David Foster Wallace gave a commencement speech at Ohio’s Kenyon College. He began:

“There are these two young fish swimming along and they happen to meet an older fish swimming the other way, who nods at them and says, ‘Morning, boys. How’s the water?’ And the two young fish swim on for a bit, and then eventually one of them looks over at the other and goes, ‘What the hell is water?’ ”

Mr. Wallace went on to say that the point of the fish story is merely that the most obvious, important realities are often the ones that are hardest to see, and to talk about.

In both life and that small subset of life known as investing, one of those realities is time. Despite its importance, time is impossible to see. It is definitely worth talking about.

How does this apply to investing? Well, investing is simply putting money aside today with a view to getting back more money after some time has elapsed.

Because invested money grows exponentially, the combination of a reasonable rate of return and the passage of time will result in a satisfying creation of wealth. Of course, the higher the rate of return, the greater the wealth creation.

Your return will increase far more dramatically with time, a factor which we too often miss.

Because we live in time in much the way that a fish lives in water, we tend to ignore it. But here’s the thing. Your rate of return over a short period of time has little effect on the ultimate amount of your wealth. It is only your average long-term rate of return that matters. If you are a competent investor and you invest in one of the better-performing asset classes, such as stocks, your very long-term average annual return is likely to fall between 6 per cent and 10 per cent.

Your time period can vary far more than your rate of return. Let’s assume your very long-term rate is 8 per cent. That will multiply your money 2.2 times over 10 years. However, it will multiply your money more than 10 times over 30 years, and more than 100 times over 60 years. And so on. It’s primarily time that drives the only return that matters.

As author Morgan Housel has succinctly put it, “Time is the exponent that does the heavy lifting, and the common denominator of almost all big fortunes isn’t returns; it’s endurance and longevity.” If you doubt this, ask yourself how Canada’s wealthiest families came to occupy that position.

Clearly, it’s important to invest, and add incrementally to your investments, at as early an age as possible – and to not interrupt the compounding of your capital.

As we all swim through the waters of time, these are ideas worth keeping in mind.

A cynic is one “who knows the price of everything and the value of nothing.” This comment, by a character in one of Oscar Wilde’s plays, does not refer to the stock market. But it serves as a good description of what happens at times like the present.

When stock market prices are rising, many investors are comfortable thinking about the intrinsic value of their investments. But when prices fall dramatically, fear causes us to focus only on recent stock prices. We are inclined to become cynical about longer-term rewards. Imagine what happens to your longer-term thinking when someone shouts “Fire!” in a movie theatre. A major price decline has the same effect on your time horizon.

Advisers and financial journalists are not immune. Their commentary switches from underlying economic value to market prices. We have now, they proclaim, “officially entered a bear market,” arbitrarily defined as a 20-per-cent drop in the stock market index from a recent high. Why is a 20-per-cent drop materially worse than a 19.5-per-cent drop? And why measure it from a recent, and possibly idiosyncratic, high point rather than, say, the price one year, or five years, ago? Your answer depends on your time horizon.

At times like this, it is worth remembering that your mindset should not change with the direction of the market. If you own stocks, you have an interest in a number of businesses. The economic value of those businesses is simply the value of all their future profits discounted to the present.

The rate at which you discount those future earnings is a function of long-term interest rates, which act like gravity on the value of all income-producing assets. This includes stocks and longer-term bonds. And particularly leveraged investments such as real estate and private equity. As long-term interest rates rise, the present value of all those assets fall. This is the principal reason for the recent stock market decline.

Naturally, the reverse occurs – that is, values rise – when long-term interest rates fall. This does not happen until the rate of inflation is expected to fall – which typically requires a period of reduced, or negative, economic growth.

All this may sound a tad pessimistic. But only to those who cannot take a longer-term view. Most of a company’s value is derived from profits that will be earned more than five years in the future. So negative growth in 2023 would have less effect on the value of future profits than you might assume. And if negative growth results in lower long-term interest rates, that will raise the economic value of all businesses.

While stock prices move up and down in the shorter term, those prices will, over time, inevitably follow the economic value of the businesses higher. In addition, you will receive some dividends along the way.

History tells us that, over the long run, North American stocks will provide a total rate of return (price appreciation plus dividends) about six percentage points greater than the rate of inflation. So, if inflation averages 3 per cent over time, that would be an average of about 9 per cent a year.

Both fees and tax will reduce that return. However, assuming you are not paying a high fee and you reduce your tax by minimizing portfolio turnover (less buying and selling of shares), your average long-term return, even after fees and tax, should be more than four percentage points above the rate of inflation. Over time, the purchasing power of your capital will increase dramatically.

The issue, of course, is the phrase “over time.” Your chances of receiving at least the return described above are good over any five-year period, and extremely good over a 10-year period. And your odds improve with every additional year. But, particularly at times like this, we are all hard-wired to think short-term. What, we ask, did the market price do over the past year or the past three months?

It is precisely these worries about short-term returns that ensure public companies usually trade at a price that gives investors the investment results described above. If prices were not volatile in the short-term, they would not provide such attractive long-term returns. Publicly traded stocks remain the single best liquid, unlevered, long-term investment.

Is this a good time to buy stocks? No one knows what the market will do over the next year, but one approach that may allow you to sleep better is to invest any new capital gradually – say, one quarter of your funds every three months.

Like Wilde, Warren Buffett has spoken of price and value. “Price is what you pay. Value is what you get.” Those who can focus on economic value rather than price will be handsomely rewarded – over time.

In a thought-provoking article last month, Globe and Mail contributor John De Goey questioned the common investing advice to “stay the course” when the stock market experiences the type of major drawdown we are now seeing. Essentially, he asked, “How can you advise people what to do when you don’t know what is going to happen?”

It is true that no one can ever know what will happen in the future. The precise outcome of any investment in stocks is always unknown. This is one of the reasons no one should invest all their money in the stock market.

For the portion of your assets you have allocated to publicly traded companies, successful investing involves thinking not in terms of certainties, but rather in terms of probabilities – based on what history has taught us. This necessarily means thinking longer-term.

You have no idea what the price of Costco, Royal Bank of Canada or Constellation Software stock will do over the next month, or even year. However, over the next 10 years, if you understand these businesses, you will likely conclude that there is a high probability their economic value will increase substantially – and that the stock price will follow so as to produce an annualized return far higher than the rate of inflation during the same period.

By thinking longer-term you are able to put the odds in your favour. You lose this advantage if you take a shorter-term view.

Mr. De Goey makes the valid point that investors are emotionally affected about twice as much by a loss as they are by a gain. In addition, people instinctively focus on what is happening right now. Psychologists have dubbed the combination of these two cognitive biases “myopic loss aversion.”

In plain English, it’s difficult for anyone, including professional investors, to watch the price of their investments decline for several weeks in a row. For that reason, many investors capitulate and sell when the market falls, presumably with the intention of investing again only when prospects appear brighter.

There are at least two problems with this approach. It’s impossible to know when the market price is about to resume its rise. And, even if you do manage to sell prior to the bottom, by the time things appear to be looking brighter, the stock price will have moved higher.

How do we know that trying to time your sales and purchases doesn’t work? That is what objective studies have shown. For example, Dalbar, an independent research firm, has compared the returns achieved by funds and investors who invest in those same funds. While the time-weighted returns were necessarily identical, the dollar-weighted returns, which reflect sales and purchases, were not. The individual investors did startlingly worse than the funds themselves because they sold when prices had fallen and bought after prices had risen. Over the 30-year period ended Dec. 31, 2021, the S&P 500 index had an annual return of 10.7 per cent whereas investors who bought a fund tracking the S&P 500 index had a return of only 7.1 per cent.

When an adviser recommends that you stay the course, she is advising you to put the odds in your favour. It’s sound advice. You should follow it.

The recently published In Pursuit of the Perfect Portfolio, by Andrew Lo and Stephen Foerster, reviews the work of 10 of the most prominent academics in the world of investing, including six Nobel laureates. They are asked to describe the investment portfolio most likely to produce the highest return combined with relatively low volatility.

Although each of these experts has a slightly different view, there is strong agreement on one point. They are unanimous that, over the long run and after fees, active investors in an efficient stock market will not be able to beat an ultra-low-fee index fund or index exchange-traded fund.

Because broad index fund products typically have less turnover (buying and selling of stocks) than actively managed portfolios, they also tend to trigger lower capital gains tax. Consequently, index products can be even more attractive on an after-tax basis – and may beat those who avoid paying a fee by making their own investment decisions.

This reality, surprising to many, has been confirmed by numerous objective studies. It is a point often made by Warren Buffett.

The most common retort by professional investors is to simply deny that it is true. To quote Upton Sinclair, “It is difficult to get a man to understand something when his salary depends upon his not understanding it.”

And it isn’t just professional investors who don’t want to hear this message. Most individual investors believe they are well above average; they resent the suggestion that their investing activities add no value.

So, does this mean that you would be better off simply investing your money in an index product?

Undoubtedly, some people would be. But there is another inconvenient truth at play here. For more than 30 years, independent investment research firm Dalbar has compared the investment return of funds and investors in those same funds. Over time, the average investor dramatically underperforms the fund in which they are invested. For example, over the 30-year period ended Dec. 31, 2021, the S&P 500 index had an annual return of 10.7 per cent whereas investors who bought funds tracking the S&P 500 had a return of only 7.1 per cent. Fees account for far less than half the difference.

How can this be? The great investor, Benjamin Graham, once said, “The investor’s chief problem – and even his worst enemy – is likely to be himself.” Emotions cause people to buy when prices are rising, and sell whenever the market price falls. Buying high and selling low has never been a formula for investment success.

Although there is no way to prove this, the tendency to panic may be less for those invested in companies. If you own TD Bank, Microsoft and Walt Disney Co., and know something about those businesses, you will understand why the economic value of those companies is likely to increase over time – with the stock price eventually to follow. Whereas, if you own an index product, it is harder to think about anything other than the price. Owning a fund may make it more likely that you will react to the volatility of the market, rather than focusing on economic fundamentals.

There are also tax planning advantages to owning individual companies. For example, if you need to sell shares to raise money, you can elect to sell those with the lowest unrealized capital gains. You can’t do this if you own a fund.

The key for individual investors who choose to own individual companies is to find a reasonable number of profitable and growing businesses, in different sectors and geographies, that appear likely to prosper for decades to come. If you have the discipline to maintain your ownership of these companies over time, you will own a basket of assets that is likely to grow, for many years to come, far faster than the rate of inflation. You will also defer the payment of capital gains tax.

The authors of In Pursuit of the Perfect Portfolio conclude that “The pursuit of the Perfect Portfolio is the foundation of financial liberty – the freedom to reach your financial goals and all the happiness it may bring.” For some, this may be achieved by owning an index fund. For others, owning a portfolio of proven companies, held for the long run, will be the road to success.

Many studies have shown that, after fees, the long-term results achieved by the majority of professional investment firms are below that of the broader stock market average. And as between individual firms, there is far less persistence of outperformance than you would guess. Given these facts, those of us in the investment management industry should be interested in improving our decision-making abilities.

Nobel Prize-winning psychologist Daniel Kahneman has dedicated his life to studying how people can make better decisions. In his highly praised 2011 book, Thinking, Fast and Slow, Dr. Kahneman described errors in human decisions arising from cognitive biases. His just published book, Noise, written with Cass Sunstein and Olivier Sibony, extends the analysis to deal with unwanted variation in judgments made by both individuals and groups.

Dr. Kahneman and his co-authors have chronicled the extraordinary level of costly mistakes, which could have been largely avoided, in areas such as medical diagnosis, insurance underwriting, bail hearings and financial forecasts. In these areas, there is often no immediate feedback as to whether a decision was correct or not. And there are few long-term studies examining the costs associated with the variability of these decisions. It is only through longer-term observation that the results of these decisions can be determined.

Not surprisingly, many of the professionals found to be committing these errors did not like having this pointed out. Why should these people, who have devoted their life to an activity, have to listen to an academic with no practical experience in the area? You might hear them say: “Those who can, do; those who can’t, write.” Typically, these decision makers chose to proceed as they always had, with their blinders firmly in place.

How does this apply to investing in the stock market? Investors (as opposed to speculators) decide whether to buy or sell a company, based on their view of whether the stock market is overestimating or underestimating the company’s future profit and, hence, its economic value. In essence, success in investing turns on the ability to accurately predict those future earnings.

Overconfidence in our ability to correctly forecast the future is one of the best documented cognitive biases. In predictive judgments, human experts are consistently outperformed by relatively simple formulas.

Despite knowing this, we are all reluctant to follow a systematic process rather than our instincts. We view today’s facts with hindsight, applying an assumed causation to everything that has happened. When we look at the past, nothing appears surprising. The result is that we expect no surprises in the future – a future that we falsely assume we can foresee accurately.

Dr. Kahneman explains how investors can improve their predictive judgments and consequently their results. Keeping an open mind – actively seeking disconfirming evidence – is extremely helpful.

So is thinking in terms of probabilities, something that is not intuitive to most of us. An example would be to take the “outside view” of a company under consideration. Investors should, for example, look at the historical rates of growth achieved by other companies of the same type and size. In trying to determine whether a business is likely to increase its revenue at 15 per cent a year for the next 10 years, it’s helpful to know how often similar businesses have (or have not) achieved that.

It is also useful, when analyzing a potential investment, to include in the analysis simple formulas or algorithms that have proven, over the long run, to be predictive of higher returns. One well-known example is the advantage of buying a company trading at a relatively low multiple of its earnings per share over the past year. There are many other relevant factors (the historical rate of growth, profitability and so on), and these can be combined. While some may choose not to rely entirely on a quantitative approach, it’s helpful to include in any analysis a systematic ranking of the companies under consideration, based on what are evaluated to be the most relevant measurements.

The authors of Noise point out that the odds of a good decision will improve if several people make entirely independent estimates and then base their decision, at least in part, on the average of the results. Having each person decide completely independently is crucial. If you had four witnesses to a crime scene, would you want them to talk to one another before testifying?

The efficacy of this “wisdom of crowds” approach has been known for many years, but is rarely followed by investment firms – in part because of a desire to avoid disagreements. It may also be easier to promote a star investment manager than a group of professionals. The authors suggest the average estimate can be treated not as the final answer, but rather as the starting point for a discussion and ultimate decision. Their advice is “don’t eliminate intuition, delay it.”

Given the proven advantage of following the procedures described above, and the cost of current practices, it is dispiriting that decision makers across professions continue to resist change.

However, for some open-minded active investment managers, Dr. Kahneman’s process may well represent the refinement needed to finally produce net results that, over the long run, do indeed outperform the stock market.

The person most responsible for China’s extraordinary economic growth over the past 50 years is Deng Xiaoping, who led that country from 1978 to 1989. His most famous quotation was a homespun comment about a distinction without a material difference. “No matter if it is a white cat or a black cat; if it can catch mice, it is a good cat.”

The investment world is rife with this type of unhelpful distinction. One of the oldest has lately had a lot of play – the distinction between value investing and growth investing.

Value investors are typically described as those who invest in companies priced inexpensively relative to their profits and assets. Growth investors are seen as those who buy fast-growing companies with less concern about the price – presumably based on their belief that the companies’ growth will skate them onside.

For stocks, this contrast has been codified in indexes such as the Russell Value Index and the Russell Growth Index. Although different organizations define growth and value in somewhat different terms, all rely upon statistical metrics such as price-to-earnings (P/E), price-to-book-value (P/B) and growth in revenue and profits.

You don’t have to think about this for very long before you realize that a company that qualifies as a value investment in one year may increase its growth in the next, potentially commanding a far higher price and becoming a growth investment.

This questionable distinction likely arose because financial academics, trained in mathematics, want to measure hard data, not apply judgment. Statistical measures, such as a P/E ratio and the percentage growth in earnings per share, qualify.

This way of thinking has gained currency in part because it allows investment firms to spin it for marketing purposes – creating new investment vehicles to differentiate themselves and gather assets. If a portion of a pension fund is currently managed by a value investor, then surely some of the fund should also be given to a growth investor to smooth out the returns. Or, given how well growth stocks have performed for the past 11 years, don’t you think it’s about time that value stocks will start to outperform?

In reality, while the contrast between value and growth may be useful for sales purposes, when it comes to improving investment returns, it is an unhelpful distinction.

To understand why, let’s go back to basics. All intelligent investing involves trying to buy an asset, be it a farm, an apartment building or a business, for a price less than its economic value. So, all rational investing is, in effect, value investing.

What is the economic value of an asset? It is simply the value of the cash that you can extract from the asset over time (excluding what you may be able to sell it for).

In the case of a business, the economic value is the future earnings, discounted back to the present. The only way to come up with an approximation of that value is to estimate those future earnings, including the rate at which they are likely to grow. As you would expect, the estimate of future growth is done, in part, by examining past growth. A business that has grown its profits at 10 per cent annually is likely to grow its future profits faster than a business that has historically grown its profits at 2 per cent annually. As Warren Buffett has said, “growth is always a component in the calculation of value.”

Here’s an example. Assume Facebook Inc. has grown its normalized earnings at more than 40 per cent a year for the past five years and is trading at 27 times what it has earned over the past 12 months (that is, it has a P/E ratio of 27). Statistically, it is a growth stock. However, an investor, who has studied the company’s economics and the sector (including regulatory risk), and formed a view of the ability of management, may conclude that it is likely to continue to grow its earnings at an attractive rate over the long run. She might conclude that today’s price represents good value. To again quote the Oracle of Omaha, value and growth “are joined at the hip.”

Determining what price to pay for a given company requires far more than simply looking at metrics based on historical data and categorizing it as a value investment or a growth investment.

Whether you are in the market for cats or companies, focus on what matters – not largely meaningless distinctions.

In Ian McEwan’s recent novel, Machines Like Me, the main character buys an advanced robot that winds up competing with him for the affections of his girlfriend while also making a quick fortune by investing in the stock market. Yikes!

While the speed of the robot’s investment success may be unrealistic, there can be no doubt that an investor able to minimize human cognitive weaknesses will outperform over time.

Three related cognitive handicaps that we, as homo sapiens, all share are: difficulty in thinking in terms of probabilities, a tendency to focus on potential losses to the exclusion of possible gains and an overconfidence in our ability to predict the future.

Successful investing, like machine learning, is based on thinking in terms of probabilities – an activity that is not intuitive for us. Instead, we tend to think in binary, all-or-nothing terms.

In order to estimate the probability of a future outcome, you require a statistically significant sample of data. When investing, this means, at a minimum, examining the relevant facts over a long time period. Typically, we don’t do that. An oft-asked question is, “What did the stock market do today?”

Also, we allow the fear of a loss to trump the likelihood of a gain. This short-term loss aversion was helpful at earlier stages of our evolution, when loss often meant serious injury or death.

The problem is that biological evolution happens extremely slowly. Our minds are hardwired for life in a state of nature, whereas we now live in far different circumstances. In today’s world, we should understand that if someone offers us a coin toss for which a correct call would win us $100 and an incorrect call would cost us $50 (half as much), we should take the bet. Most people will not.

When someone says, “I’d rather be safe than sorry,” it strikes most of us as prudent. If we still lived on the savannah among lions, it would be. However, when it comes to investing capital over the long run, it is typically those who have chosen the perceived safety of cash or bonds who are ultimately sorry – or would be if they compared their return to that of the broad stock market.

Another of our human weaknesses is a stunning overconfidence in our ability to predict the future better than others. As the great Canadian-born economist J.K. Galbraith said, “There are two kinds of forecasters: those who don’t know and those who don’t know that they don’t know.” Most of us fall into the latter category.

When it comes to investing, this overconfidence causes otherwise intelligent people to think they can “time the market,” an activity that is guaranteed to lower your long-term return.

How do you avoid these cognitive weaknesses? Well, if you are a tax-paying individual and wish to do your own investing, here is a simple, but not necessarily easy, approach.

Set aside, in short-term cash equivalents such as GICs, a buffer account to cover your expenses for one to two years. Invest the balance of your capital in an ultralow-fee global stock index fund or ETF, one that represents all global markets, including the emerging economies.

And then leave your investments alone! As Warren Buffett has wisely said about investing, “Inactivity strikes us as intelligent behaviour.”

A combination of real economic growth, inflation and dividend payments will ensure that you will – over time – receive a safe and highly satisfactory return from global stocks. Inactivity is likely to improve your before-tax return and is extremely likely to improve your after-tax return.

However, not touching your investments will be difficult for most people.

It may assist you in staying the course to remember that the price assigned by the stock market to a group of companies will fluctuate around the growing economic value of those companies. The market price is also far more prone to short-term volatility than the economic value. So, more often than not, if the market price falls, your future percentage gain has increased.

This simple approach may not beat an advanced robot, but over time it should outperform most human investors.

In economics, interest rates act as gravity behaves in the physical world. At all times, in all markets, in all parts of the world, the tiniest change in rates changes the value of every financial asset. You see that clearly with the fluctuating prices of bonds. But the rule applies as well to farmland, oil reserves, stocks, and every other financial asset. – Warren Buffett

These days, people often ask, “Why is the U.S. stock market up when the economy is shrinking?”

Perhaps surprising to most people, the stock market almost always ignores current economic conditions. As columnist Nir Kaissar, writing for Bloomberg, has pointed out, from 1930 to 2019, the correlation between annual changes in real U.S. GDP and annual real returns for the S&P 500 Index was 0.09. In other words, there was no correlation.

So, what does determine the price of stocks? In the short run, it is market sentiment, which is always unpredictable. Over time, however, share prices reflect the economic value of the underlying businesses.

The economic value of each business is simply all of its future profits discounted to today. And for the stock market, it is the weighted average of the economic values of all of its publicly traded businesses. If you find this answer both highly theoretical and based on an unknown future, we agree with you. It is, however, a helpful framework for understanding how stock prices will move over time.

Let’s talk about discounting those future profits, which is where interest rates come in. A $1-million profit earned 10 years from now is worth less than the same amount earned this year. How much less? Well, that depends on how much you can earn, at a risk-free interest rate, over the same period.

When the long-term rate on government bonds is 2 per cent, a business’ future earnings are worth almost 50 per cent more than when that rate is 6 per cent. So, long-term interest rates have a major influence on the economic values of businesses and, therefore, their share prices.

When people ask why the market is up, they are often really asking, “Is the market overvalued?” Two common tests for overvaluation or undervaluation are the price-earnings ratio of the market and the ratio of the market’s overall capitalization to GDP. Today, both of these measures, taken alone, point to a relatively expensive stock market.

This is, however, in part because long-term rates are at historic lows. The 10-year U.S. treasury yield is now about 0.7 per cent – well down from even a year ago. More importantly, because of the high level of government debt worldwide, it is unlikely that governments will allow interest rates to move up significantly in the next several years.

You can be sure that Mr. Buffett is not spooked by the shrinking economy. He is, instead, taking advantage of short-term volatility to find attractive investments for the long run.

If you invest a sum of money at 10 per cent for five years, you will multiply your wealth by 1.6 times.

If you invest your capital at that rate for 10 times as long (50 years), you will not multiply your wealth by 16 times.

You will multiply it by more than 117 times.

Does this strike you as surprising? It should, because exponential growth (also known as compound growth) is difficult for the human mind to grasp.

Understanding it, however, is the wellspring of successful investing. Albert Einstein is reputed to have said, “Compound interest is the eighth wonder of the world. He who understands it, earns it; he who doesn’t, pays it.”

Let’s go back to basics. Investing is simply putting a sum of money away for a period of time with a view to receiving back significantly more money, in real terms, in the future.

Your success as an investor is a function of two things:

What determines your long-term rate of return? Studies have shown that by far the most important factor is the asset class you invest in. Investing in a portfolio of growing businesses, through ownership of publicly traded or private companies, will produce the highest unleveraged return.

The only return that matters is your long-term return, and, for most asset classes, your long-term investment return is reasonably predictable. History teaches us that, over 20 or more years, assuming inflation is reasonably muted, your average annual return from investing in a portfolio of listed companies (stocks) is likely to be between 7 per cent and 10 per cent, before taxes.

Any tax paid on your investment return will, of course, reduce this. This is one of the few certainties in investing. Investors are taxed on their capital gains only when the asset is sold. There is, therefore, a huge advantage to holding each of your investments for the long run. As Warren Buffett has said, “Tax-paying investors will realize a far, far greater sum from a single investment that compounds internally at a given rate than from a succession of investments compounding at the same rate.”

Almost everyone focuses more on the rate of return than on the length of time for which their capital will be invested. However, to benefit from compound growth, it is essential to think about both factors – and your ability to change the investment time period is far greater than your ability to change the long-term rate of return. “Buy right and hold tight” is a slogan adopted by some of the world’s most successful investors.

This hold-for-the-long-run approach explains why almost all the world’s great family fortunes (think Buffett, Gates, Thomson) have been created by owning shares in a growing business over many decades, thereby allowing their value to compound over time on a before‐tax basis.

There is, however, a limitation on how long individuals can compound their wealth tax-free. On your death, you are, for tax purposes, deemed to have disposed of your investments. Consequently, your estate is taxed on your capital gains up to that date. So, for individual stockholders, buy and hold works best if you live to be as old as Methuselah.

Companies, however, do not suffer from mortality. If you own your investments through a company that you control through fixed value preferred shares, and set it up so the common shares are held by a trust for your children or grandchildren, you avoid paying capital gains tax on your death. A good tax accountant can help you with this.

The power of long-term compounding, and the fact that it is counterintuitive, are at the heart of why some investors become very wealthy over time – and most do not.

Studies have shown that, when it comes to investing, most people make decisions based on intuition rather than reasoning. They focus primarily on the possibility of a loss (rather than the probability of a gain), and tend to contemplate the immediate future rather than taking a long-term view.

Together, these behavioural biases drive people to invest a disproportionate share of their capital in an asset class that makes absolutely no sense for long-term investors – particularly in today’s environment. That asset class is bonds.

At this point, you may be thinking that bonds are far less risky than stocks and, therefore, they have a place in every portfolio. It is true that, in the short-run, the market price of bonds tends to be less volatile than the market price of stocks. Thus, the idea of a “balanced” portfolio, consisting of both stocks and bonds, sounds wonderfully comforting.

The more you think about it, however, the less comforting it becomes.

Let’s go back to basics. Investing is laying out money now in the expectation of receiving more money, in real terms, well into the future. The phrase “in real terms” refers to the inevitable decline in the purchasing power of a dollar, because of inflation. In Canada, it takes about $1.46 today to buy what $1 did 20 years ago. The inflation rate over this time period was about 1.9 per cent per annum.

If, over the past 20 years, you owned a portfolio of 10-year Government of Canada bonds, you received an average yield of 3.6 per cent a year. If you paid tax at a 50-per-cent marginal rate, your bonds would, after tax, have produced an annual return of 1.8 per cent – less than the rate of inflation. So, after both tax and inflation, you would have lost money.

In addition, any increase in longer-term interest rates will result in a fall in the market value of bonds. The longer the remaining term to maturity of the bonds, the greater the sensitivity of market price to changes in interest rates. One cynic has said that instead of providing risk-free returns, bonds actually provide return-free risk.

For most people, the obvious alternative investment to bonds is stocks. While a bond is simply an interest-bearing IOU from the issuer of the bond to the investor, a stock is a piece of ownership in a business. An investment in a productive asset such as a business should, unlike a bond, be able to deliver profits that will keep up with or exceed inflation. Stocks should, therefore, over time, represent a better investment than bonds.

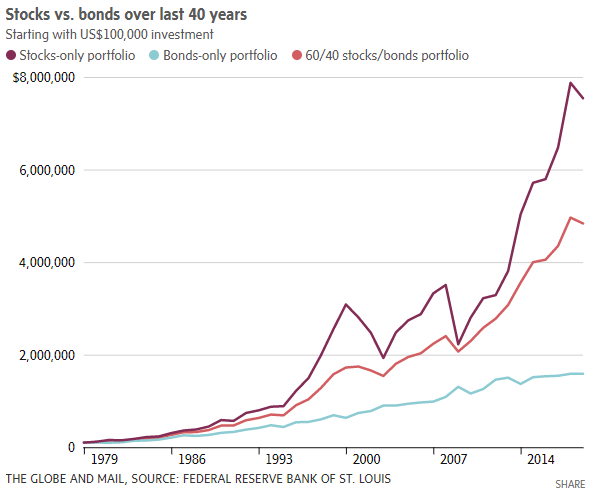

If we are right about this, it should show up when we examine the total long-term returns on stocks and bonds. The U.S. numbers (provided by the Federal Reserve database) are more complete than the Canadian equivalents and include a broader range of sectors. We looked at three portfolios over the past 40 years, each valued on Jan. 1, 1979 at US$100,000. The first contained the stocks in the S&P 500 Index, the second consisted of the return on U.S. 10-year Treasury bonds and the third was a balanced portfolio with a typical weighting of 60-per-cent stocks and 40-per-cent bonds, rebalanced annually.

While stocks were more volatile, the stock portfolio finished well ahead. By Dec. 31, 2018, the value of the bond portfolio reached US$1.59-million. The balanced portfolio rose to US$4.84-million. And the stock portfolio finished at US$7.54-million (more than four times the value of the bonds). The same would be true over almost any long-term period.

Looking at a long time period such as 40 years is important. It provides statistically relevant data, which enables you to more accurately estimate the likely outcome of any action you might take. Also, your ability to live comfortably will depend on the return provided by your investments for the rest of your life. This includes your retirement, which is likely to last more than 20 years. Cash flow obtained from a combination of dividends and realized capital gains is taxed at a far lower rate than interest from bonds.

So, what is the argument for owning bonds? Primarily, peace of mind. While experienced investors know that short-term fluctuations in the price of stocks are to be expected and tolerated, those fluctuations cause angst for most of us.

How should we minimize this angst? In our view, not by investing in a so-called balanced portfolio of stocks and bonds. Rather, we suggest you invest an amount equal to, say, three years of estimated living expenses in a “buffer” account that holds short-term cash equivalents such as one-year guaranteed investment certificates.

Unlike a portfolio of bonds, the value of your GICs will not fluctuate with interest rates. If you are taking funds from your investment account to cover living expenses, withdrawals can be made from this buffer account. The buffer account can be topped up from the stock portfolio each January, so long as your stocks have performed well the previous year. After a down year in the stock market (which happens about one in four years), you can delay the top-up until things improve. Maintaining the buffer account will, of course, reduce the long-term return on your assets. But the peace of mind it provides may make it worthwhile.

Choosing the right asset class is your most significant investment decision. Those who get it right will be rewarded with a far more comfortable retirement.

Studies of investment returns reveal a startling paradox. Over time, the vast majority of professional investors will produce an after-fee return that is below that of the broader stock market. However, certain financial formulas relating to public companies can be used to produce substantial outperformance over the long run.

Why is this and how can we learn from it?

To back up a little, the distinction here is between two schools of investing – usually referred to as fundamental and quantitative. While the approaches are radically different, it is possible to combine the best aspects of each.

Fundamental investing is what most investors, including professionals, do. You examine a company, often in depth, predict how the business will do in the future, estimate whether the company is undervalued or overvalued by the market and buy or sell accordingly. Success depends on your ability to predict the company’s future profits better than the other market participants.

Quantitative investing typically involves a large portfolio and high turnover. The approach is somewhat counterintuitive. It does not rely on predictions of the future. Derived from academic research, and enabled by large amounts of data, it is based on the proven correlation between certain financial information about companies (referred to as factors) and higher investment returns. Most of this financial information is readily available on the internet.

To take a well-known example involving a value factor, many studies have shown that if you had, 50 years ago, simply measured the ratio of price per share to earnings per share (the P/E ratio) for each company in the stock index and then bought only the 10 per cent of companies having the lowest P/E ratio – and adjusted your portfolio once a year in accordance with this rule – you would have substantially outperformed the market over the long run. If you had added a few other factors that have also been proven to coincide with higher returns, you would have done even better.